Much of the industry banter surrounding rounds growth has been attributed to the perfect storm created by the COVID 19 pandemic. And with a renewed caution in the air, driven by the Delta variant, it is not surprising to us to see the industry sustain robust participation data throughout the Summer 2021 season. Our ongoing Back to Normal Barometer research continues to pulse golfer and overall U.S. consumer attitudes and behaviors. With the latest wave of research, we continue to observe how several COVID related phenomena have directly and positively impacted the rounds growth and bullish attitudes about the present state of golf participation. It has been widely documented how golf has been able to successfully position itself as one of the few viable options for outdoor recreation and socialization, particularly during the more restrictive, peak waves of the pandemic. As golf facility operators and other stakeholders continue to ponder the sustainability of the surge in participation that the sport has enjoyed since last Summer, these latest developments, while perhaps alarming for the nation as a whole, bode well for the golf industry.

Much of the industry banter surrounding rounds growth has been attributed to the perfect storm created by the COVID 19 pandemic. And with a renewed caution in the air, driven by the Delta variant, it is not surprising to us to see the industry sustain robust participation data throughout the Summer 2021 season. Our ongoing Back to Normal Barometer research continues to pulse golfer and overall U.S. consumer attitudes and behaviors. With the latest wave of research, we continue to observe how several COVID related phenomena have directly and positively impacted the rounds growth and bullish attitudes about the present state of golf participation. It has been widely documented how golf has been able to successfully position itself as one of the few viable options for outdoor recreation and socialization, particularly during the more restrictive, peak waves of the pandemic. As golf facility operators and other stakeholders continue to ponder the sustainability of the surge in participation that the sport has enjoyed since last Summer, these latest developments, while perhaps alarming for the nation as a whole, bode well for the golf industry.

Amplifying the bullishness are two new phenomena that we are now observing that have potentially longer term implications. First, is the struggle that other leisure activities have had in ramping back service levels and delivering on desired customer experiences. As the first chart above illustrates, less than half of the population has experienced what we’ve dubbed as a “COVID Liberation Moment”… defined as a particular moment in time where for someone, personally, they felt that they had basically gotten their pre-pandemic life back in some meaningful way, either temporarily or permanently. If golf has been a viable substitute and/or taken on greater resonance over the past seventeen months, it does not appear that it has been knocked down from such a perch.

Amplifying the bullishness are two new phenomena that we are now observing that have potentially longer term implications. First, is the struggle that other leisure activities have had in ramping back service levels and delivering on desired customer experiences. As the first chart above illustrates, less than half of the population has experienced what we’ve dubbed as a “COVID Liberation Moment”… defined as a particular moment in time where for someone, personally, they felt that they had basically gotten their pre-pandemic life back in some meaningful way, either temporarily or permanently. If golf has been a viable substitute and/or taken on greater resonance over the past seventeen months, it does not appear that it has been knocked down from such a perch.

Adding to this observation is the fact that nearly six in ten feel that the resumption of normal activities limited during the height of the pandemic, have been underwhelming, relative to one’s expectations and recollections. The chart above further shows that a substantial segment of people have been underwhelmed by the return of non-golf, “competitive” leisure activities. Clearly, at least for the short term, the return of other previously coveted non-golf activities has failed to impress.

A second phenomenon that may have even longer term positive implications for golf, is a foundational shift that we are finding in work patterns. The pandemic has taught many businesses to pivot to hybrid and work from home models. There has been ever growing pushback from employers towards a return to the workplace, and the next chart (right), shows a steady decline in those working strictly from home. However the split time hybrid model has more than held its own, particularly among golfers. If this workplace model becomes the new normal, or even maintains itself as a formidable and prevalent situation, we can comfortably surmise that the implications for golf will be a positive, as flexible schedules allow greater latitude for those who’ve embraced golf to continue to participate at heightened levels.

The final piece contributing to our bullish expectation for sustained rounds participation is a direct result of the COVID belt tightening that we are again seeing as we move towards the Fall. Couple the hybrid work phenomenon with the delayed re-opening of workplaces, and conditions remain ripe for us to continue to ride the COVID wave through the balance of 2021. You’ll see (left) that nearly one in 5 golfers won’t return to the office before 2022, if at all. And golfer sentiments are much in favor of such a scenario. It’s no surprise then, that the participation numbers reported by others, remain robust through the early portion of the Summer.

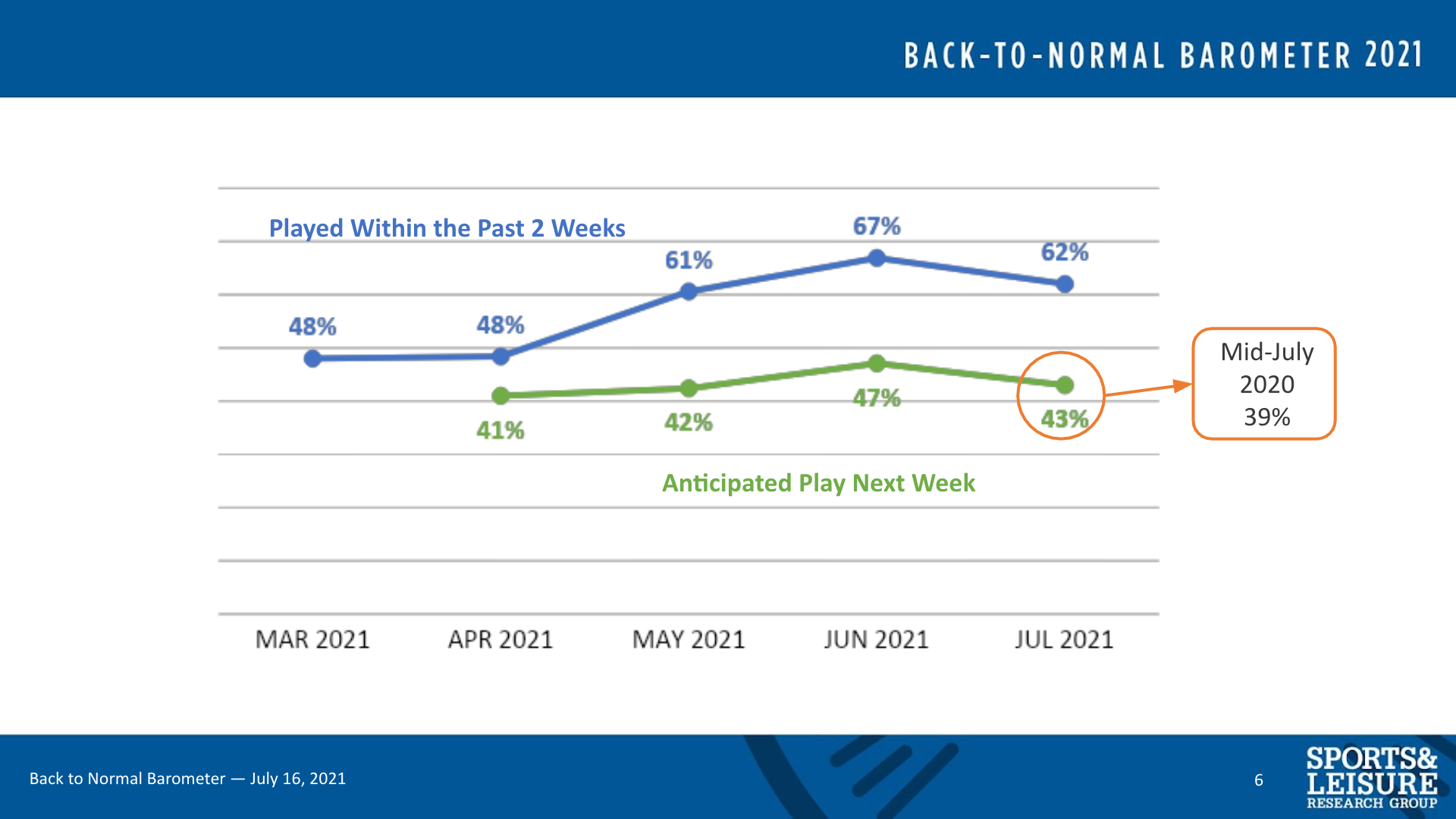

Our Back to Normal Barometer tracking (right) of more short term/close-in participation and expectation remain steady with what we reported last month and continue to show a positive outlook in the near term future and relative to where we were a year ago. The party isn’t over yet for those facility operators who can exploit these opportunities and tap into the current golfer mindset.

Our Back to Normal Barometer tracking (right) of more short term/close-in participation and expectation remain steady with what we reported last month and continue to show a positive outlook in the near term future and relative to where we were a year ago. The party isn’t over yet for those facility operators who can exploit these opportunities and tap into the current golfer mindset.

To see more timely, business-critical data from Sports and Leisure Research Group and other industry experts and leaders, head to NGCOA's Research Center.